By Neil Cooper-Smith, senior analyst, Business Pilot.

February’s figures suggest the market is beginning to settle into a clearer rhythm after January’s seasonal reset. While the new year often brings a surge of early enquiries followed by cautious decision-making, February shows signs of strengthening momentum: particularly in sales performance and order values.

Conversion rates stabilised, remaining consistent at 38.7%, compared to January’s 38.4%. While still below December’s peak, this stabilisation is important. January often sees a temporary dilution as fresh enquiries enter the pipeline, but February’s small recovery indicates that those early-year prospects are now progressing more decisively. In context, this reflects a market that is not overheating but quietly consolidating.

Lead activity softened slightly compared to January, easing by around 8%. That cooling is not unusual after the sharp post-Christmas rebound and does not suggest weakening demand. In fact, when viewed alongside the sales data, it points to a healthier funnel: fewer speculative enquiries, but stronger intent among those who do make contact.

That intent is most evident in sales volumes, which increased by approximately 11% month-on-month. This marks a second consecutive rise and signals that installers are successfully converting opportunity into confirmed work. Importantly, sales growth has now outpaced lead growth, reinforcing the idea that February was less about volume and more about efficiency and quality of engagement.

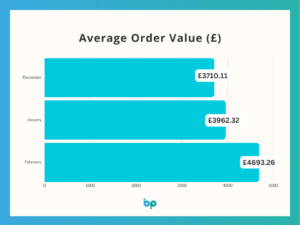

Average order values rose significantly again in February, increasing by nearly 18% to £4,694, compared to January’s £3,962; this represents a meaningful acceleration in spend per project. Rather than trading down, homeowners appear willing to commit to higher-value installations. That pattern suggests confidence among those proceeding, even if broader consumer sentiment remains measured.

The wider UK economic backdrop helps to explain this measured but positive progression. The rate of inflation dropped to 3% in the year to January, down from 3.4% in December, moving closer to the Bank of England’s 2% target.

Meanwhile, interest rates remained at 3.75% in February, significantly lower than their 2024 peak, with further gradual reductions expected across the year. Stabilised borrowing costs are particularly supportive for younger homeowners and those with mortgages coming up for renewal, improving affordability for larger discretionary purchases.

At the same time, UK wage growth has remained ahead of inflation, gradually restoring purchasing power, and consumer confidence – while still negative overall – has shown incremental improvement since the start of the year.

These factors in tandem – easing inflation, stabilising interest rates, and real wage growth – create a cautiously supportive environment for home improvement investment.

For installers, the implication is clear: February was less about chasing sheer enquiry volume and more about capitalising on committed buyers. In an environment where overall confidence is improving slowly rather than surging, success depends on understanding which opportunities are ready to convert and ensuring follow-up is timely and targeted.

This is where tools like Business Pilot become particularly valuable. By tracking conversion trends, monitoring order value shifts, and analysing pipeline movement in real time, installers can focus effort where it delivers the greatest return. When demand is selective rather than universal, precision matters more than ever.

As we move into March, February’s data suggests the foundations for 2026 are steady. Growth is not explosive, but it is structured, value-driven, and increasingly efficient. For businesses that remain data-led and responsive, that is a platform worth building on.